Industry, construction, manufacturing, energy — the forces underneath markets that most financial media ignores. Analysis and tools built to operate inside them.

Analysis on industry, construction, energy, and capital flows — delivered free, every week. No noise. No prediction. Just structure.

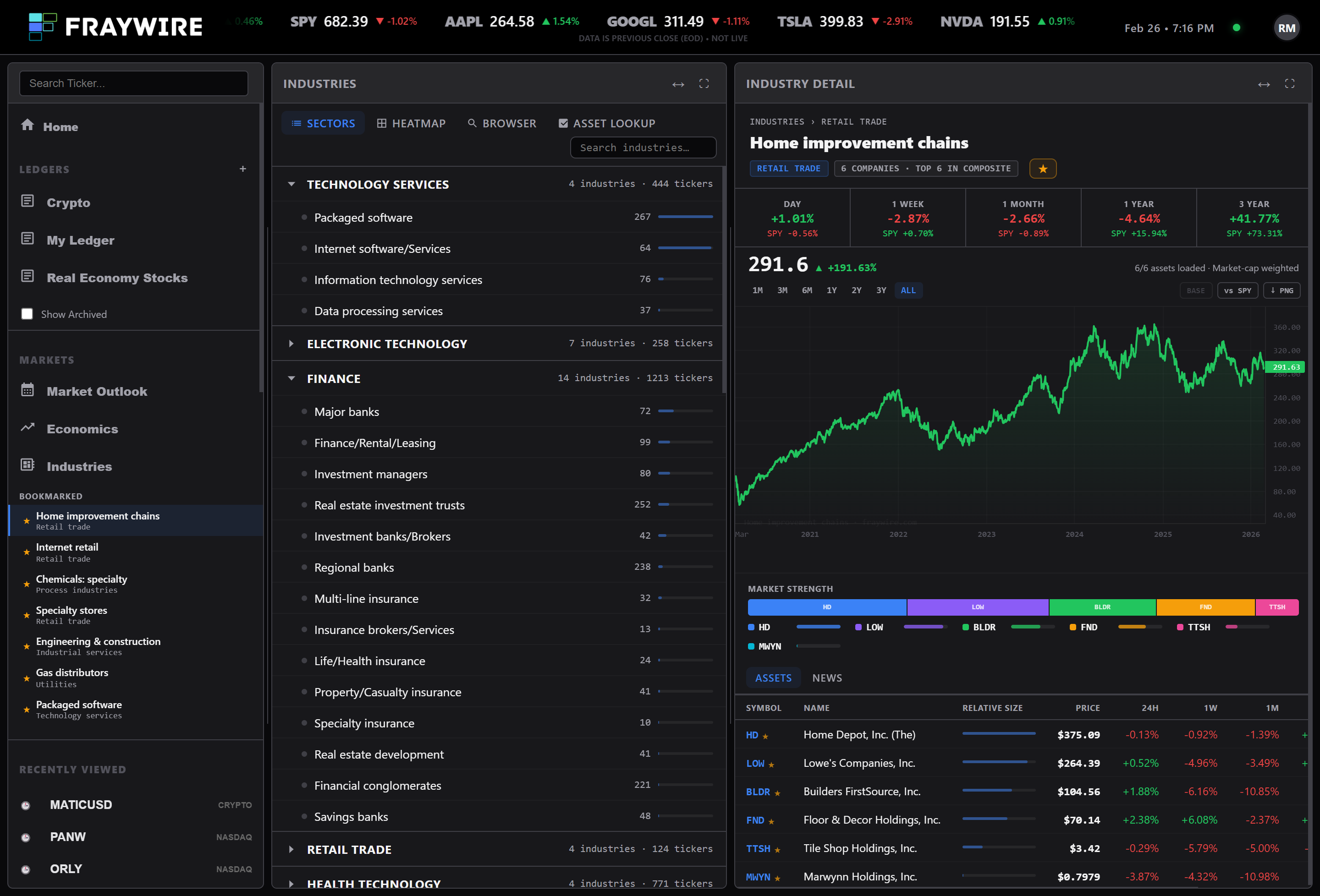

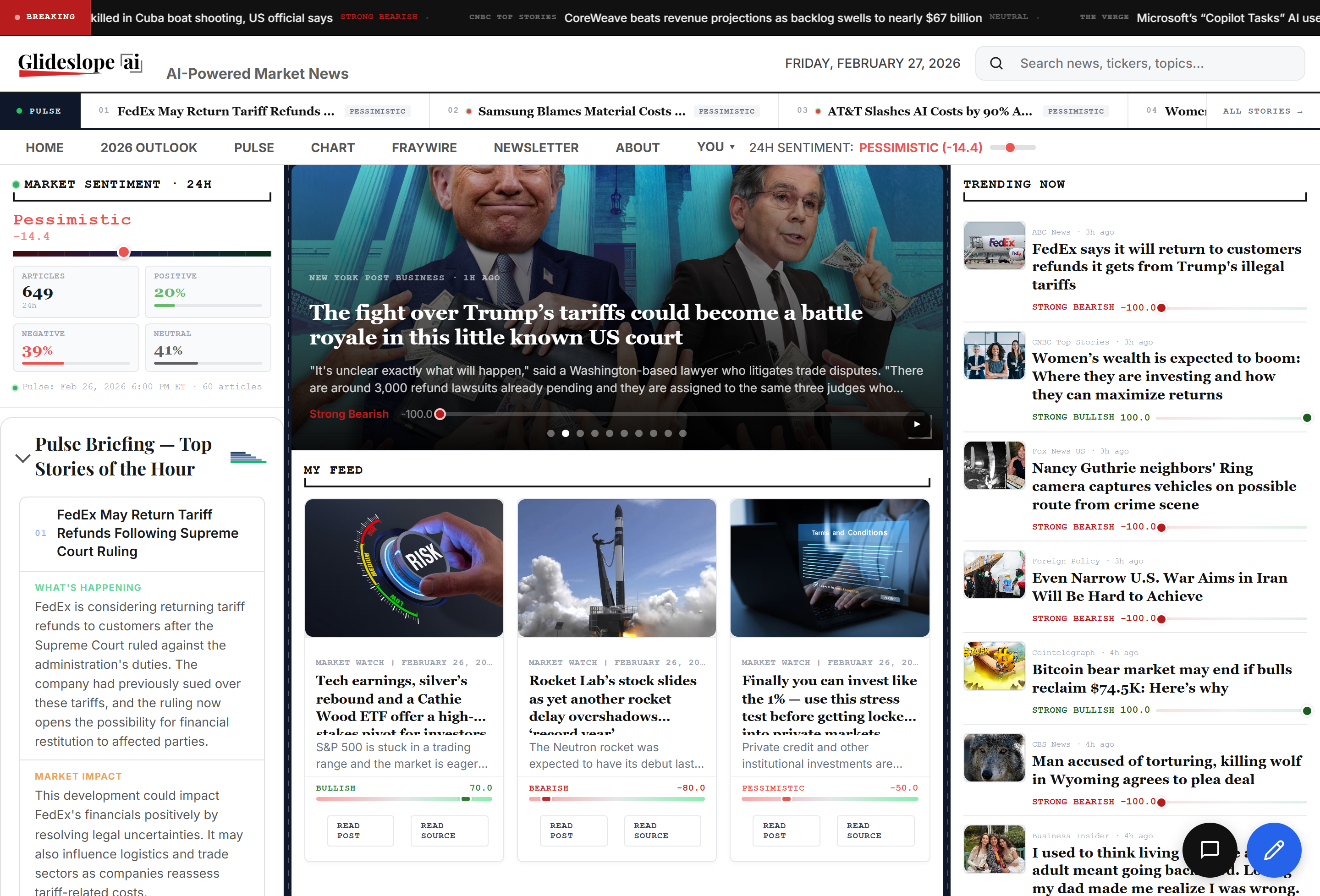

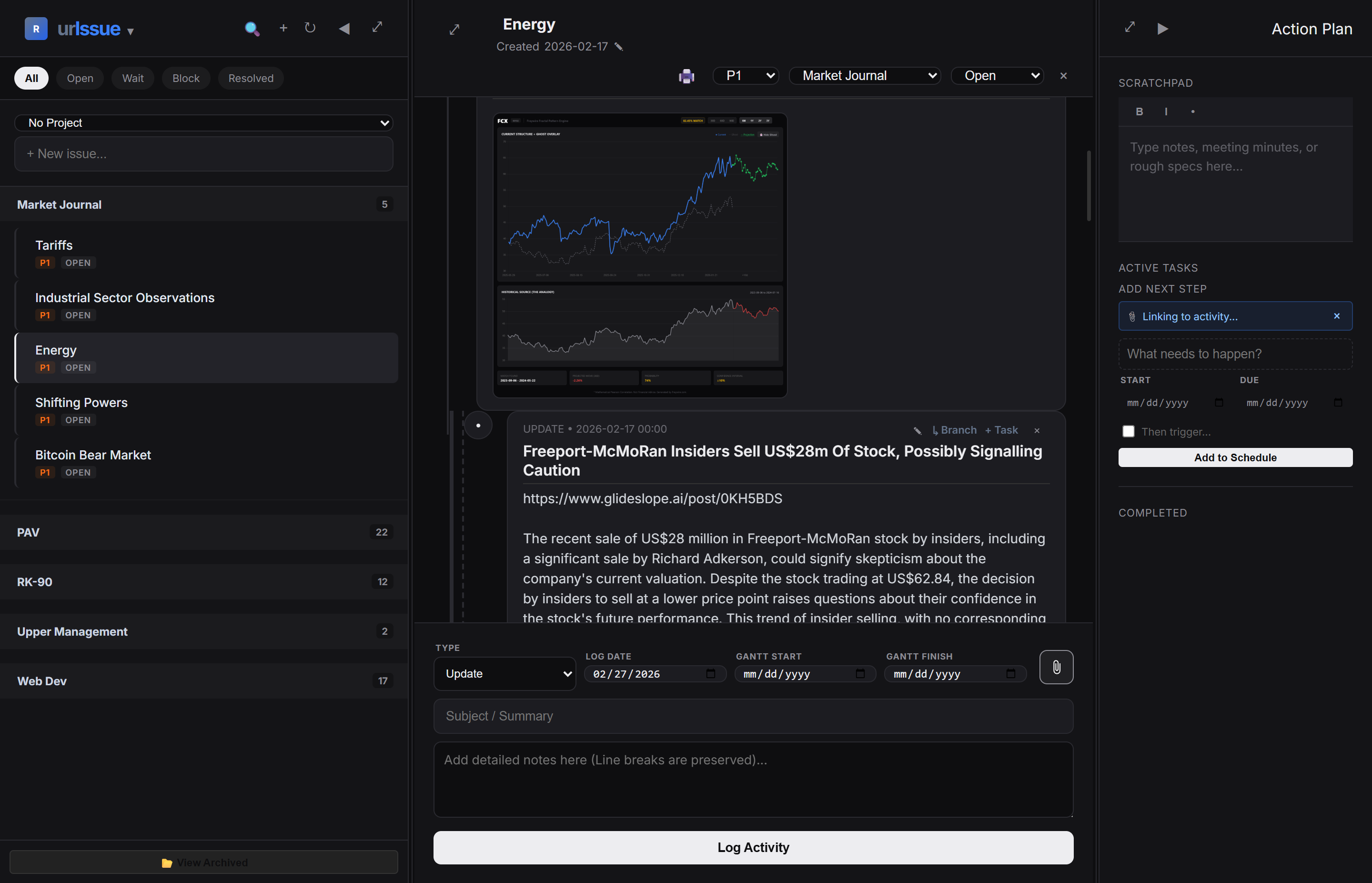

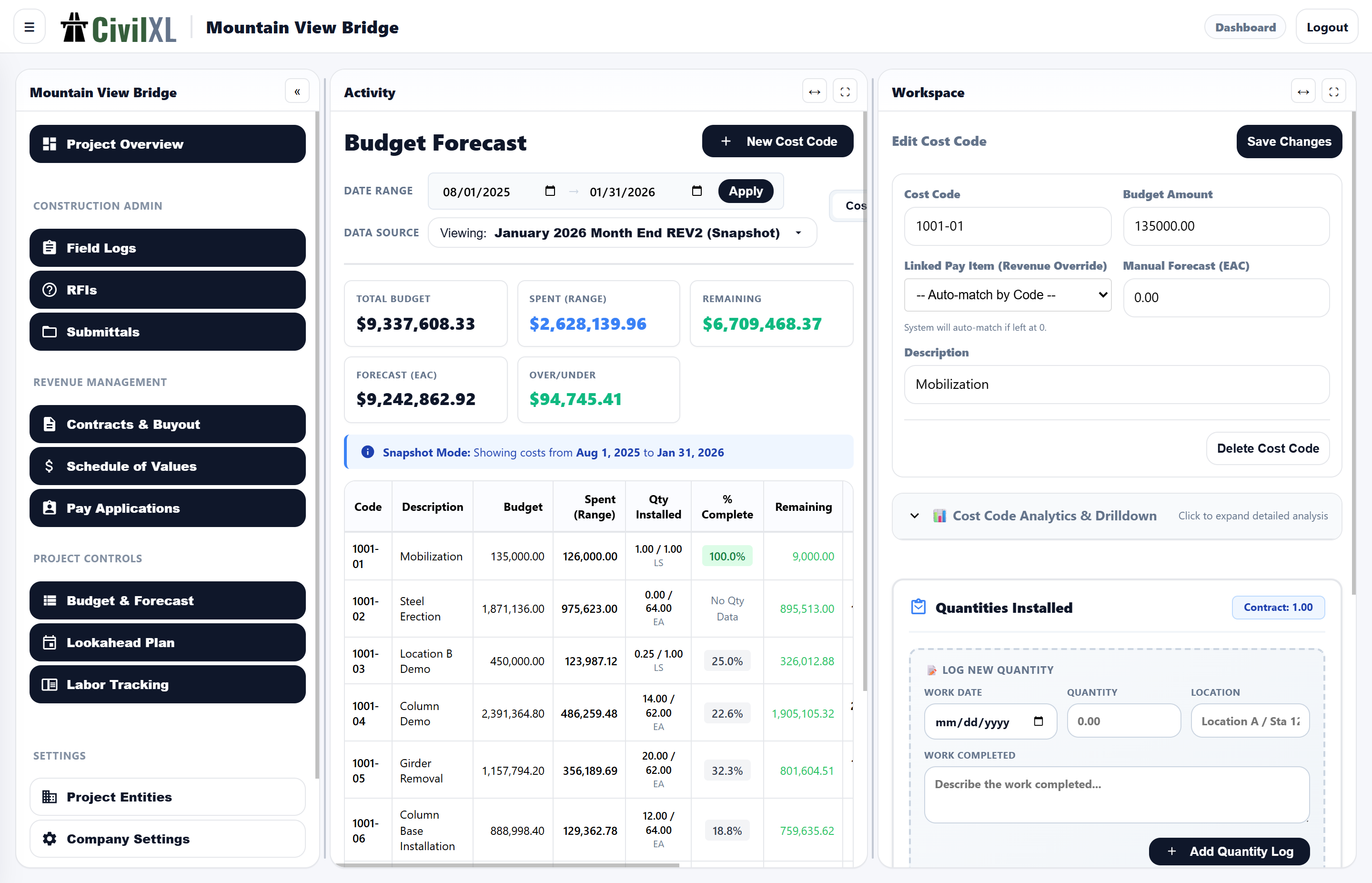

Four tools built for the real economy — from market data and news intelligence to project operations and construction management.

Fraywire, Glideslope, urIssue, and CivilXL — under a single subscription. First 30 days free. Cancel any time.

No credit card required to start.

An independent intelligence operation that tracks the forces that move money before prices adjust.

The focus is mechanics on the real economy: infrastructure, construction, manufacturing, and energy. Breaking Metrics explores the data and strategies behind what makes these markets make or break.

Alongside the newsletter, Breaking Metrics builds tools. Fraywire for market and economic data, Glideslope for news intelligence, urIssue for project operations, and CivilXL for construction management. All four platforms are built for builders.