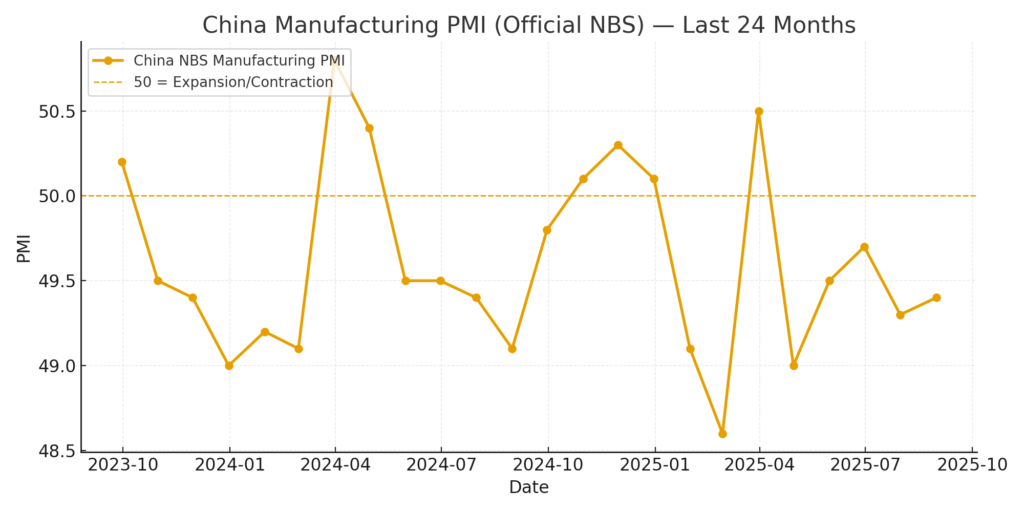

China’s latest data offered another red flag for the global economy. The country’s official manufacturing PMI came in at 49.4 for August, marking the fifth straight month of contraction. At the same time, U.S.–China trade tensions are dragging on, with tariff threats and stalled talks casting a shadow over markets. Together, these forces are reverberating through industries, supply chains, and portfolios worldwide.

China’s Weak Manufacturing Pulse

A PMI reading below 50 signals contraction. Despite a marginal uptick from July’s 49.3, August’s 49.4 highlights that China’s industrial economy remains under stress. Demand at home is hampered by the property downturn, while exports are cooling as Western consumers cut back.

- Electronics, machinery, and chemicals all show soft orders.

- Small and medium manufacturers are reporting tighter margins due to higher financing costs and weaker demand.

- Beijing has extended its trade truce with Washington by 90 days, but negotiations are going nowhere fast.

China’s factory PMI is stuck in contraction — a warning sign for global demand.

The industrial slowdown isn’t just cyclical; property and credit stress make it structural.

The Industries Most Exposed

Certain global sectors are tightly wired into China’s cycle:

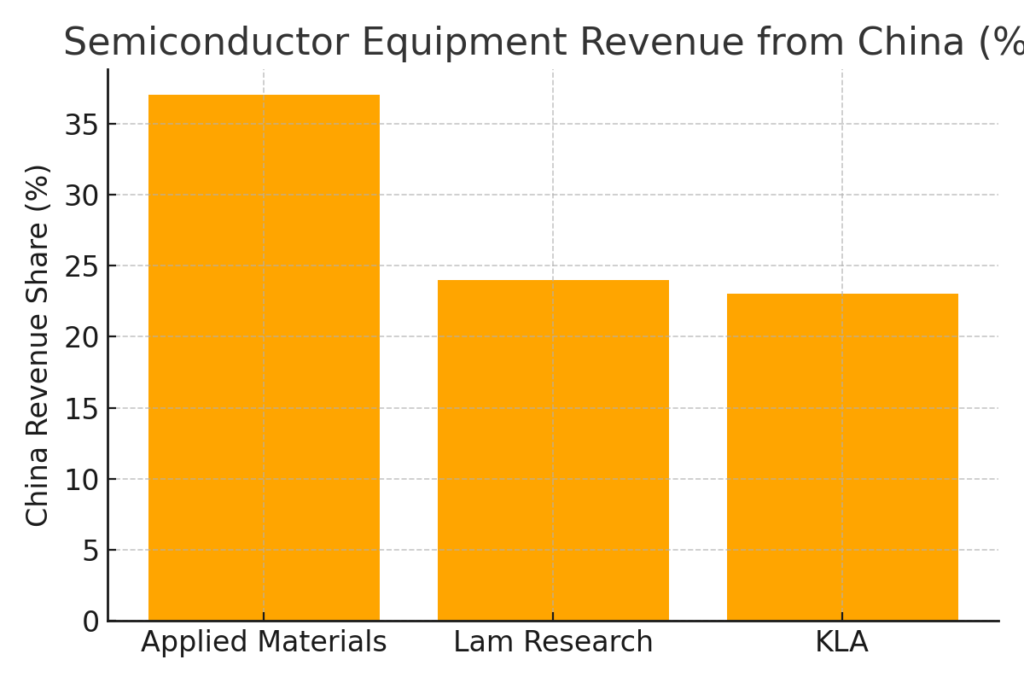

- Semiconductors & chip equipment: U.S. firms like Applied Materials, Lam Research, and KLA face licensing hurdles shipping tools to Chinese fabs.

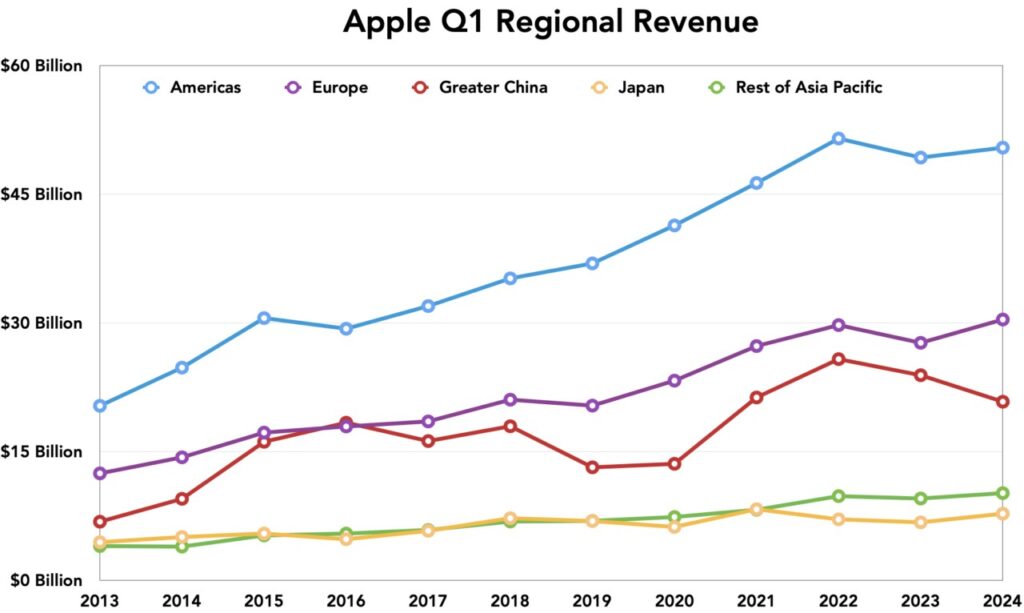

- Electronics & smartphones: Apple’s “Greater China” sales remain a major revenue slice; weak consumer demand or tariffs weigh heavily.

- Autos & EVs: Tesla’s Shanghai Gigafactory is its largest production hub, while Western automakers depend on Chinese buyers. Meanwhile, China’s dominance in batteries (≈90% cathode, >97% anode) underpins the global EV rollout.

- Solar & clean tech: Over 80% of solar module production remains China-centric, leaving U.S. and European energy projects vulnerable to cost spikes.

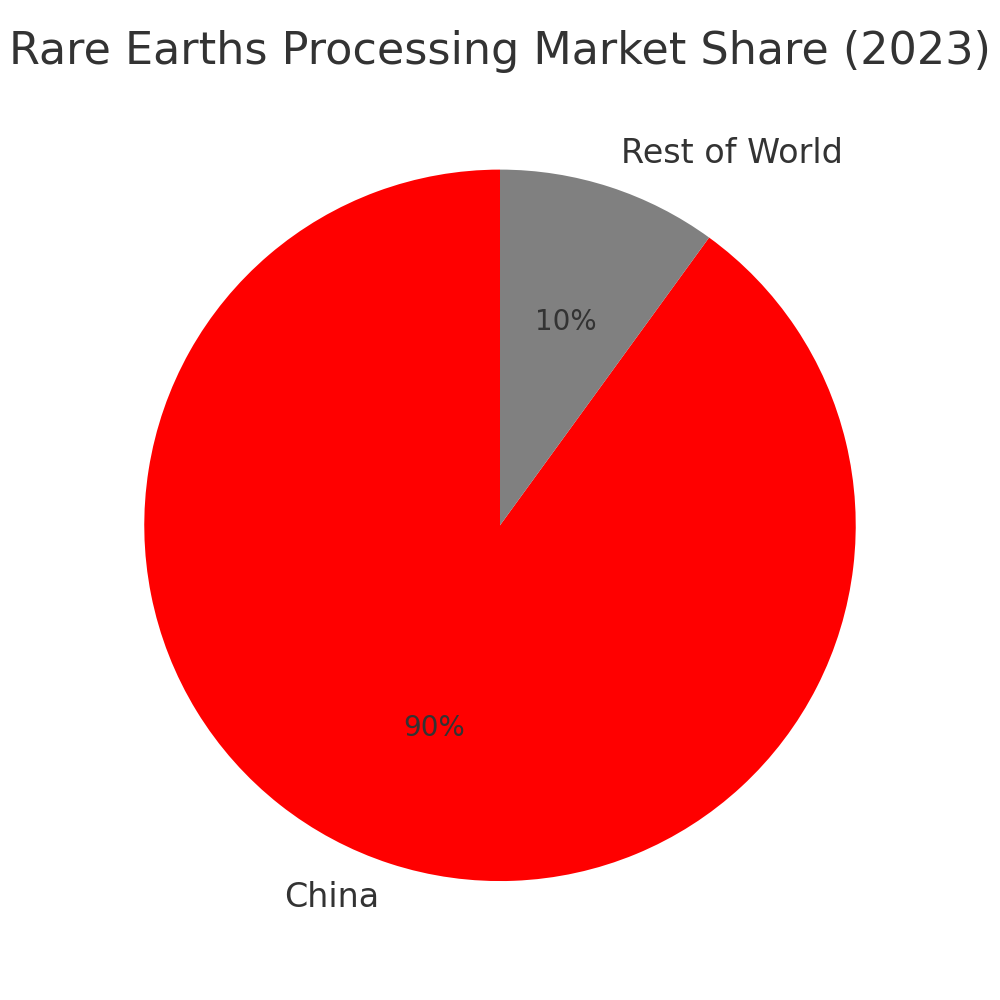

- Rare earths & minerals: China refines ~90% of rare earths, crucial for EVs, wind turbines, and defense.

- Consumer & leisure: Slowing Chinese demand dents luxury (LVMH, Kering) and Macau-exposed casinos (Wynn, Las Vegas Sands, MGM).

- Commodities: China consumes half the world’s copper; weakness drags miners like Freeport-McMoRan.

Chip gear, Apple, Tesla, and copper miners = frontline casualties.

Solar, EVs, and rare earths tie the clean-energy transition to China.

Luxury and casinos mirror Chinese consumer confidence.

U.S.–China Interconnection: De-Risking, Not Decoupling

While headlines talk about “decoupling,” the reality is more nuanced:

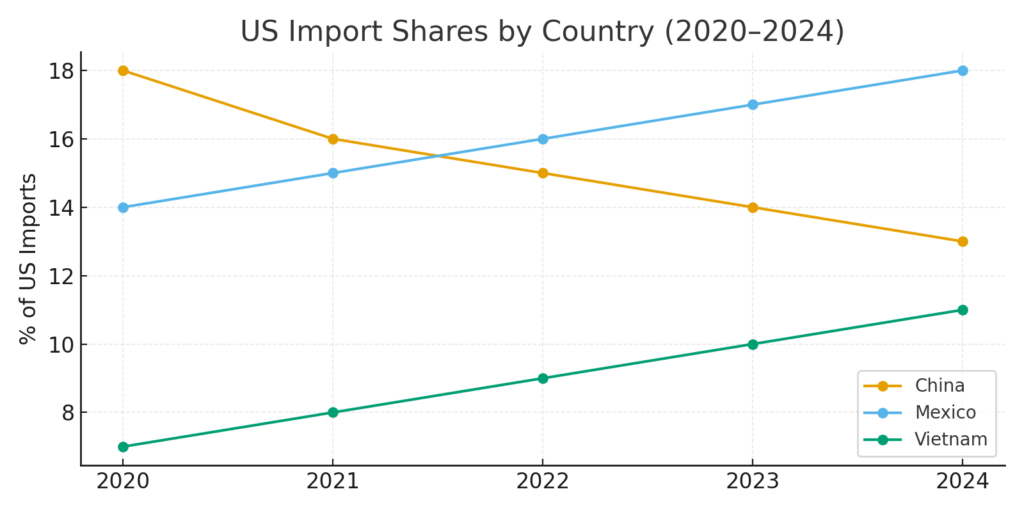

- Trade: China is still the U.S.’s third-largest goods partner, with >$200B in trade so far this year. Mexico and ASEAN nations are taking share, but U.S.–China flows remain huge.

- Finance: China holds $756B in U.S. Treasuries (June 2025), down from its peak but still significant.

- Supply chains: Solar modules, batteries, and rare-earths are overwhelmingly China-dependent — there’s no quick substitute.

- Currency: The yuan has stayed stable between 7.15–7.35 per dollar this year, reflecting Beijing’s commitment to avoid FX turmoil.

Talk of “decoupling” oversells it — supply chains and finance remain locked together.

Mexico and Vietnam are picking up U.S. imports, but inherit tariff risks.

A stable yuan = less currency shock, more long-term chess.

Global Ripple Effects

This isn’t just a U.S.–China story — the world feels it:

- Europe: German automakers lose share to Chinese EVs, while luxury houses (LVMH, Hermès) depend on Asian demand.

- Emerging Asia: Vietnam, Malaysia, and Mexico benefit from “China-plus-one” diversification, but risk U.S. tariff penalties as re-routing hubs.

- Commodities: Chile’s copper, Australia’s iron ore, and Gulf oil exports swing with Chinese demand.

- Clean energy: Tariff fights or supply hiccups in China ripple straight into the costs of EV and solar rollouts worldwide.

EU autos and luxury brands are indirect China plays.

Mexico/ASEAN win factories but inherit tariff headaches.

Copper, iron ore, and oil exporters are China barometers.

Clean-energy costs hinge on Chinese inputs — tariffs risk slowing the green transition.

The Market Lens

Despite tariffs and PMI weakness, U.S. equities have been resilient. The S&P 500 is up double digits year-to-date, powered by strong earnings, rate-cut hopes, and optimism that tariff-driven inflation will be fleeting. But beneath the surface, sectors with China exposure are diverging sharply.

- Bullish sentiment hinges on a Fed rate cut later this month.

- Any escalation in trade frictions or further Chinese weakness could trigger rotation into defensive assets.

Markets are betting tariffs = temporary; earnings + Fed cuts = durable tailwinds.

But China-exposed sectors (chips, EVs, luxury) are canaries in the coal mine.

Final Word

China’s factory slump is more than a local story — it’s a global pulse check. Industries from chips to copper, iPhones to iron ore, are caught in the middle. De-risking is real, but decoupling is myth. And until global supply chains truly diversify, a sub-50 PMI in Beijing will keep echoing across Wall Street, Frankfurt, and Santiago alike.

Socials

X:https://x.com/breakingmetrics

Instagram:https://www.instagram.com/breakingmetrics

Substack:https://substack.com/@breakingmetrics

Stay ahead of the markets. Subscribe to Breaking Metrics for in-depth analysis on key levels, sentiment trends, and the forces shaping stocks, crypto, and the economy. Fraywire+ Members get insights like this before anyone else. Don’t miss a beat—subscribe today, for free.

The information provided in this newsletter is for educational and informational purposes only. It does not constitute financial, investment, legal, or tax advice. The content is not personalized to the needs, objectives, or financial situation of any individual reader. All investments carry a high level of risk, including the potential for loss of principal. The market analysis, predictions, and opinions expressed are based on the information available at the time of writing and should not be considered as a guarantee of future performance.

Please conduct your own research and due diligence before making any investment decisions. It’s advisable to consult with a qualified professional regarding your specific circumstances before taking any action based on the information presented here. The author and publisher of this article disclaim any liability for any direct or incidental loss incurred by applying any of the information in this article, including but not limited to, any loss or damages resulting from errors, omissions, or inaccuracies in the information provided. Remember that past performance is not indicative of future results.

Stay ahead of news and sentiment with www.glideslope.ai.