Trump’s tariff gambit shows that volatility isn’t collateral damage — it’s foreign policy.

Tariffs Are No Longer Temporary

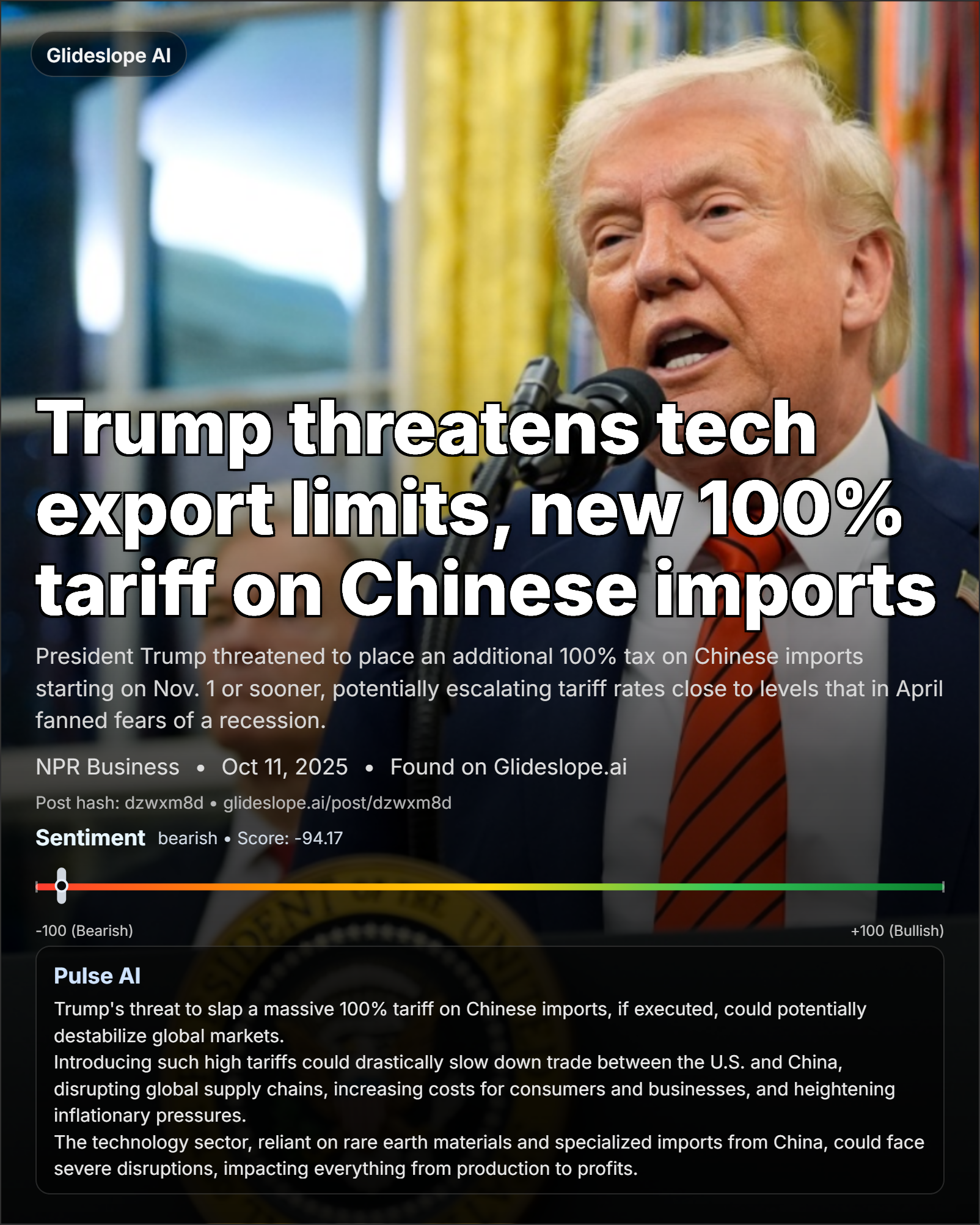

Trump’s latest 100 % tariff threat wasn’t improvisation — it was the next step in a year-long escalation. China’s decision to restrict rare-earth exports cornered Washington politically, and Trump responded in the only way his administration knows how: visibly and forcefully. Tariffs have evolved from tactical bargaining chips into a standing policy framework.

Markets initially treated these episodes as noise. But after April’s near-bear-market collapse, investors understand that tariff risk is systemic, not situational. What changed Friday wasn’t the policy — it was the market’s acceptance that this is the new regime.

Tariffs are no longer shocks; they’re structure. Investors now trade within policy risk, not around it.

What Markets Were Really Pricing

Friday’s sell-off told a subtler story than headlines suggested. Bond yields fell instead of rising, and inflation expectations barely moved. The market wasn’t fearing higher prices — it was fearing lower visibility. The move was a repricing of confidence, not of inflation.

In short: this was about trust, not CPI.

When politics hijack predictability, capital seeks safety. That’s why Treasuries rallied even as equity volatility spiked — investors shifted toward instruments that feel immune to tweets and tariffs.

This wasn’t an inflation scare; it was a credibility shock. Policy unpredictability, not macro data, now drives volatility.

The Panic Is Just Noise

Friday’s sell-off wasn’t about economics — it was about emotion.

When traders hear “100 % tariffs,” the reflex is to imagine a 1930s-style collapse. But the U.S. market isn’t a fragile export engine; it’s a self-contained machine fueled by liquidity, buybacks, and an ever-expanding monetary base. The nominal value of equities keeps rising because the denominator — the dollar itself — keeps stretching. What looks like growth is often just currency drift, and that’s precisely why moments like this feel worse than they are.

The truth is, policy shocks fade quickly in an economy where financial assets are the policy. Liquidity finds a home. Capital adjusts. A week from now, the same traders who panic-sold on tariffs will be bidding the dip, rationalizing that inflation hedge assets — equities, real estate, even Bitcoin — benefit from the same monetary dynamics they fear.

The market doesn’t need calm to rise; it just needs liquidity and time. Both remain abundant.

This panic isn’t fundamental — it’s reflexive. In an inflationary system, markets expand faster than fear can contract them. The tariff shock will pass; liquidity endures.

Why Trump Had to Act

For Trump, this was as much political necessity as economic maneuver. China’s rare-earth chokehold directly threatens U.S. industrial and defense capacity. Doing nothing would have looked weak; tariffs projected strength.

They also fit neatly into the domestic narrative of re-industrialization and “America First 2.0.” The tariffs are both deterrent and campaign message — signaling power abroad while feeding populist confidence at home.

Markets may dislike uncertainty, but Washington sees volatility as leverage. Every spike in the VIX is also a reminder to Beijing that U.S. consumer demand remains a weapon.

Volatility is now a tool of statecraft. The administration views market shock as bargaining capital, not collateral damage.

What Happens Next

The setup for the next several weeks is a tug-of-war between policy aggression and market resilience.

The Fed remains dovish, liquidity is abundant, and corporate balance sheets are healthy — all of which cushion downside momentum. The most likely path is a choppy recovery led by defensives, energy, and domestic-facing sectors. Tech and import-reliant industries will lag until the tariff path clarifies.

Our base case: the S&P 500 rebounds toward 6,500–6,700 by early November, but volatility stays sticky. The “buy-the-dip” reflex will still work — it’ll just come with a higher risk premium.

Expect a noisy rebound, not a new bull run. Liquidity still wins the short game, but politics now sets the tempo.

The Broader Shift

The deeper transformation underway is psychological. For a decade, markets were trained to see central banks as the ultimate stabilizers. That era is over. Now, the stabilizer is the uncertainty itself — a higher baseline of risk that investors must permanently price in.

We’ve entered a regime where politics, not policy rates, dictate cycles. Fundamentals still matter, but only until the next headline hits.

The market has a new master variable: politics. Tariffs are just the instrument — uncertainty is the yield curve.

Final Outlook

Policy risk is now a feature, not a bug.

Trump’s tariffs didn’t create chaos; they confirmed it as the default setting.

Expect rotation, elevated volatility, and markets that no longer trade on earnings alone. The age of data-driven markets is ending.

The policy era has begun.

Socials

X:https://x.com/breakingmetrics

Instagram:https://www.instagram.com/breakingmetrics

Substack:https://substack.com/@breakingmetrics

Stay ahead of the markets. Subscribe to Breaking Metrics for in-depth analysis on key levels, sentiment trends, and the forces shaping stocks, crypto, and the economy. Fraywire+ Members get insights like this before anyone else. Don’t miss a beat—subscribe today, for free.

The information provided in this newsletter is for educational and informational purposes only. It does not constitute financial, investment, legal, or tax advice. The content is not personalized to the needs, objectives, or financial situation of any individual reader. All investments carry a high level of risk, including the potential for loss of principal. The market analysis, predictions, and opinions expressed are based on the information available at the time of writing and should not be considered as a guarantee of future performance.

Please conduct your own research and due diligence before making any investment decisions. It’s advisable to consult with a qualified professional regarding your specific circumstances before taking any action based on the information presented here. The author and publisher of this article disclaim any liability for any direct or incidental loss incurred by applying any of the information in this article, including but not limited to, any loss or damages resulting from errors, omissions, or inaccuracies in the information provided. Remember that past performance is not indicative of future results.

Stay ahead of news and sentiment with www.glideslope.ai.